Getting the big welcome

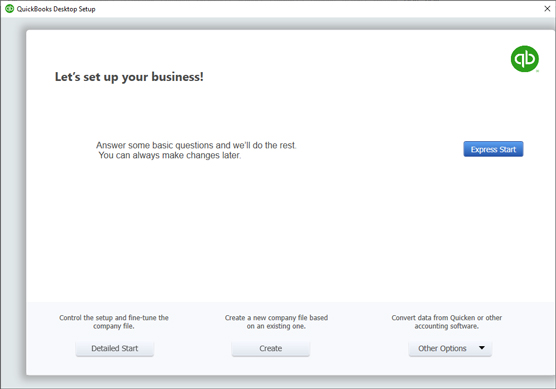

The Let’s Set Up Your Business! screen of QuickBooks Setup (see the figure) appears when you choose File→New Company. The screen gets you started on providing some general information about setting up a new company within QuickBooks. You probably want to read this screen’s information. When you’re ready to begin, click the Express Start button or the Detailed Start button. The QuickBooks Setup window, showing the welcome message

The QuickBooks Setup window, showing the welcome messageThe Express Start method

QuickBooks provides an accelerated version of the QuickBooks setup process, which you can use when you don’t want to customize setup. If you click the Express Start button, QuickBooks collects a bit of information about your company and, based on that information, sets up a company file that should work for a business like yours.After you click Express Start to create the company file, QuickBooks prompts you to describe the people (customers, vendors, and employees) you do business with, the items you sell, and your bank account. You provide these descriptions by stepping through a series of screens and filling in onscreen boxes and worksheets.

The Detailed Start method

The Detailed Start button, if clicked, starts the EasyStep Interview, which walks you through a bunch of screens full of information that let you rather tightly specify how the company file that QuickBooks sets up should look.To move to the next screen in the EasyStep Interview, click the Next button. To move to the previous screen, click the Back button. If you get discouraged and want to give up, click the Leave button. But try not to get discouraged.

Supply company information

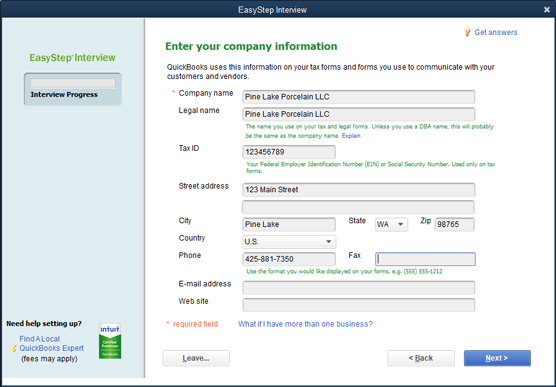

The first few screens of the EasyStep Interview collect several important pieces of general information about your business, including your company name and the firm’s legal name, your company address, the industry in which you operate, your federal tax ID number, the first month of the fiscal year (typically, January), the type of income tax form that your firm uses to report to the IRS, and the industry or type of company that you’re operating (retail, service, and so forth). The first screen of the EasyStep Interview is shown. The first screen of the EasyStep Interview collects general company information.

The first screen of the EasyStep Interview collects general company information.QuickBooks isn’t very smart about the tax accounting rules for limited liability companies (LLCs). An LLC can be treated as a sole proprietorship if it has one owner and as a partnership if it has more than one owner. But LLCs may also elect to be treated as S corporations or C corporations. If you’ve made such an election for your LLC, be sure to indicate that the LLC is an S corporation or C corporation.

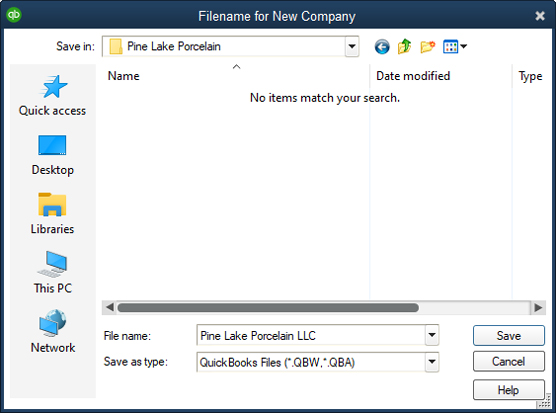

After collecting this general company information, QuickBooks creates the company data file that stores your firm’s financial information. QuickBooks suggests a default name or a QuickBooks data file based on the company name. All you need to do is accept the suggested name and the suggested folder location (unless you want to save the data file in the Documents folder, which isn’t a bad idea). The Filename for New Company dialog box

The Filename for New Company dialog boxCustomizing QuickBooks

After QuickBooks collects the general company information mentioned in the preceding paragraphs, the EasyStep Interview asks you some very specific questions about how you run your business so that it can set the QuickBooks preferences. Preferences, in effect, turn various accounting features of QuickBooks on or off, thereby controlling how the program works and looks. Here are the sorts of questions that the EasyStep Interview asks to set the QuickBooks preferences:- Does your firm maintain inventory?

- Do you want to track the inventory that you buy and sell?

- Do you collect sales tax from your customers?

- Do you want to use sales orders to track customer orders and back orders?

- Do you want to use QuickBooks to help with your employee payroll?

- Do you need to track multiple currencies within QuickBooks because you deal with customers and vendors in other countries, and do these people regularly have the audacity to pay or invoice you in a currency different from the one your country uses?

- Would you like to track the time that you or your employees spend on jobs or projects for customers?

- How do you want to handle bills and payments (enter the checks directly, or enter the bills first and the payments later)?

How to set your start date

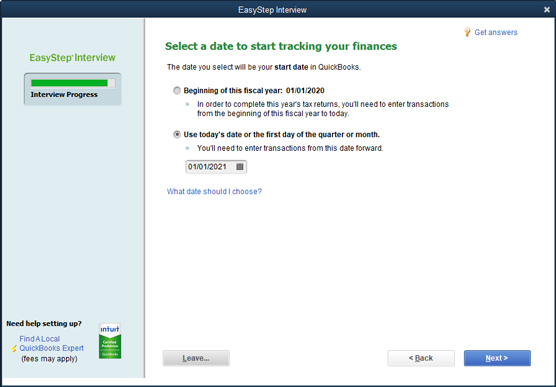

Perhaps the key decision that you make in setting up any accounting system is the day on which you begin using your new system. This day is called the conversion date. Typically, you want to begin using an accounting system on the first day of the year or the first day of a new month. Accordingly, one other big question you’re asked is about the conversion date. You’re prompted to identify the start date by using the dialog box shown. The EasyStep Interview dialog box that lets you select the start date

The EasyStep Interview dialog box that lets you select the start dateThe easiest time to start using a new accounting system is the beginning of the year. The reason? You get to enter a simpler trial balance. At the start of the year, for example, you enter only asset, liability, and owner’s equity account balances.

At any other time, you also enter year-to-date income and year-to-date expense account balances. Typically, you have this year-to-date income and expense information available only at the start of the month. For this reason, the only other feasible start date that you can pick is the start of a month.In this case, you get year-to-date income amounts through the end of the previous month from your previous accounting system. If you’ve been using Sage 50 Accounting, for example, get year-to-date income and expense amounts from Sage.

After you’ve provided the start date, supplied the basic company information, identified most of your accounting preferences, and identified the date on which you want to start using QuickBooks, you’re almost done.

If you click the Leave button, QuickBooks leaves you in the QuickBooks program, ready to get to work. The EasyStep Interview process isn’t lost forever, however. To get back into the interview, just open the file you were in the process of setting up. When you do, the EasyStep Interview restarts.

Review the suggested chart of accounts

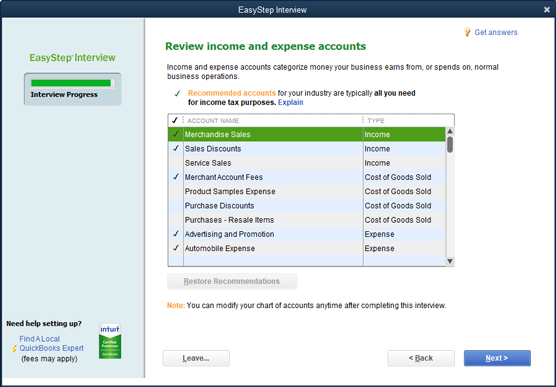

At the very end of the EasyStep Interview, based on the information that you supply about your type of industry and the tax return form that you file with the IRS, QuickBooks suggests a starting set of accounts, which accountants call a chart of accounts. These accounts are the categories that you use to track your income, expenses, assets, liabilities, and owner’s equity. This figure shows the screen that the EasyStep Interview displays for showing you these accounts. The EasyStep Interview screen shows you its recommended income and expense accounts.

The EasyStep Interview screen shows you its recommended income and expense accounts.The accounts that QuickBooks marks with a check, as the screen explains, are the recommended accounts. If you don’t do anything else, these checked accounts are the ones you’ll use (at least to start) within QuickBooks. You can remove a suggested account by clicking the check mark. QuickBooks removes the check mark, which means the account won’t be part of the final chart of accounts. You can also click an account to add a check mark and have the account included in the starting chart of accounts.

You can click the Restore Recommendations button at the bottom of the list to return to the initial recommended chart of accounts (if you made changes that you later decide you don’t want).

When the suggested chart of accounts looks okay to you, click Next. It’s fine to accept what QuickBooks suggests because you can change the chart of accounts later.Add your information to the company file

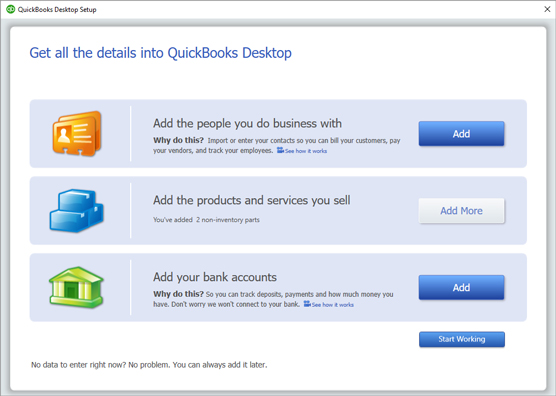

No matter whether you use the Express Start method of creating a company file or the Detailed Start/EasyStep Interview method, after you and QuickBooks set up the company file, QuickBooks prompts you to enter your own information in the company file. The QuickBooks Setup screen that prompts you to enter your own information in the company file

The QuickBooks Setup screen that prompts you to enter your own information in the company fileCustomers, vendors, and employees

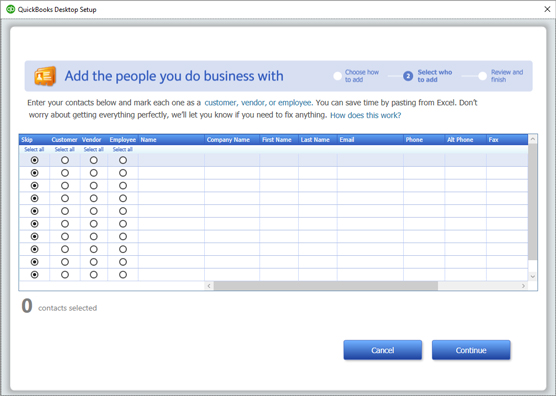

To describe customers, vendors, and employees, click the first Add button. QuickBooks asks whether it’s possible to get this data from someplace else, such as an email program or email service (Outlook, Gmail, and so forth), or whether you want to enter the information into a worksheet manually. You’re probably going to enter the information manually, so click the appropriate button and then click Continue. When QuickBooks displays a worksheet window (see the following figure), enter each customer, vendor, or employee in its own row, and be sure to include both the name and address information. Click Continue (not shown) when you finish. Then QuickBooks asks (using a screen I don’t show here) whether you want to enter opening balances — amounts you owe or are owed — for customers and vendors. Indicate that you do by clicking the Enter Opening Balances link and then enter the opening balances in the screen that QuickBooks provides. The QuickBooks Setup screen collects information about the people you do business with.

The QuickBooks Setup screen collects information about the people you do business with.Services and inventory items you sell

To describe the stuff you sell, click the second Add button. QuickBooks asks about the stuff you sell — whether you sell services, whether you sell inventory items, and whether you want to track any such inventory items you sell, for example. Answer these questions by clicking the option button that conforms to your situation and then click Continue.When QuickBooks displays a worksheet window (not shown), describe each item you sell on a separate worksheet row. Also be sure to describe any inventory items you’re holding at the time you convert to QuickBooks. Click Continue when you finish. If you sell more than one type of item, you need to repeat this process for each type of item.