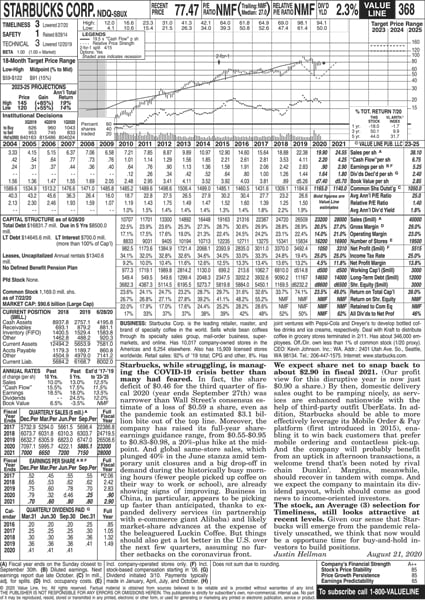

The beauty of Value Line’s service is that it condenses the key information and statistics about a stock (and the company behind the stock) to a single page. Suppose you’re interested in investing in Starbucks, the retail coffeehouse operator. You’ve seen the stores, and you figure that if you’re going to shell out more than $4 or $5 for a cup of their flavored hot water, you may as well participate in the profits and growth of the company. You look up the recent stock price and see that it’s about $85 per share.

Take a look at the important elements of the Value Line Investment Survey page for Starbucks.

Reprinted by permission; all rights reserved. Value Line, The Value Line Investment Survey, Timeliness, and Safety are trademarks or registered trademarks of Value Line Inc. and/or its affiliates in the United States and other countries. Copyright by Value Line, Inc.

Reprinted by permission; all rights reserved. Value Line, The Value Line Investment Survey, Timeliness, and Safety are trademarks or registered trademarks of Value Line Inc. and/or its affiliates in the United States and other countries. Copyright by Value Line, Inc.Value Line Investment Survey report on Starbucks.

The information in Value Line’s reports is in no way insider information. Look at these reports the same way that you review a history book: They provide useful background information that can keep you from repeating common mistakes.

1. Business

This section of the report describes the business(es) that Starbucks participates in. You can see that Starbucks is the largest retailer of specialty coffee in the world. Although 92 percent of the company’s sales come from retail, note that 8 percent come from other avenues — such as mail-order, online, and supermarket sales. You also find details about joint ventures, such as Starbucks’ partnerships with Pepsi and Dreyer’s to develop and sell bottled coffee drinks and ice creams, respectively. This section also shows you what portion of the company’s stock is owned by the senior executives and directors of the company (less than one percent in this case); seeing that these folks have a financial stake in the success of the company and stock is a good thing.2. Analyst assessment

A securities analyst (in this case, Justin Hellman) follows each Value Line Investment Survey stock. An analyst focuses on specific industries and follows a few dozen stocks. This section of the Value Line report provides the analyst’s summary and commentary of the company’s current situation and future plans.3. Value Line’s ratings

The Value Line Investment Survey provides a numerical ranking for each stock’s Timeliness (expected performance) over the next year. One is highest and 5 is lowest, but only about 5 percent of all stocks receive these extreme ratings. A 2 rating is above average and a 4 rating is below average; about one-sixth of the ranked stocks receive each of these ratings. All remaining stocks — a little more than half of the total ranked — get the average 3 rating.The Safety rating works the same way as the Timeliness rating, with 1 representing the best and least volatile stocks and the most financially stable companies. Five is the worst Safety ranking; it denotes the most volatile stocks and least financially stable companies.

Starbucks’ current ratings are 3 for Timeliness, which is average, and 1 for Safety, which is well above average. I’ve never been a fan of predictions and short-term thinking. (One year is a very short period of time for the stock market.) However, historically, Value Line’s ranking system has held one of the best overall track records according to the Hulbert Financial Digest, which tracks the actual performance of investment newsletter recommendations. Even so, you shouldn’t necessarily run out and buy a particular stock because of its high ranking. Just keep in mind that higher-ranked stocks within the Value Line Investment Survey have historically outperformed those without such ratings.

4. Stock price performance

The graph in the figure shows you the stock price’s performance over the past decade or so. The highest and lowest points of the line on the graph indicate the high and low stock prices for each month. At the top of the graph, you see the year’s high and low prices. Starbucks stock has risen significantly since the company first issued stock in 1992, but like all stocks, Starbucks has experienced some down or sideways periods. (The small box in the lower-right corner of the graph shows you the total return that an investor in this stock earned over the previous one, three, and five years and compares those returns to the average stock.)The graph also shows how the price of the stock moves with changes in the company’s cash flow (money coming in minus money going out). The solid line in the Starbucks graph represents 19.5 times the company’s cash flow. Over time, just as stock prices tend to track corporate profits, so, too, should they generally follow cash flow.

Cash flow is an important measure of a company’s financial success and health — it’s different from net profits, which the company reports for tax purposes. For example, the tax laws allow companies to take a tax deduction each year for the depreciation (devaluation) of the company’s equipment and other assets. Although depreciation is good because it helps lower a company’s tax bill, subtracting it from the company’s revenue gives an untrue picture of the company’s cash flow. Thus, in calculating a company’s cash flow, you don’t subtract depreciation from revenue.

5. Historic financials

This section shows you 12 to 18 years of financial information on the company (in the case of Starbucks, you get information going back to 2004). The two most helpful pieces of information in this section are:- Book value per share: This number indicates the value of the company’s assets, including equipment, manufacturing plants, and real estate, minus any liabilities. Book value gives somewhat of a handle on the amount that the company can sell for if it has a “going-out-of-business sale.” I say somewhat because the value of some assets on a company’s books isn’t correct. For example, some companies own real estate, bought long ago, that is worth far more than the company’s current financial statements indicate. Conversely, some manufacturers with equipment find that if they have to dump some equipment in a hurry, they need to sell the equipment at a discount to entice a buyer.

The book value of a bank, for example, can mislead you if the bank makes loans that won’t be paid back, and the bank’s financial statements don’t document this fact. All these complications with book value are one of the reasons full-time, professional money managers exist. (If you want to delve more into a company’s book value, you need to look at other financial statements, such as the company’s annual report.)

- Market share: For some companies (not Starbucks), the Value Line Investment Survey also provides another useful number in this section of the report: the market share, which indicates the portions of the industry that the company has captured in a given year. A sustained decline in a company’s market share is a dangerous sign that may indicate its customers are leaving for other companies that presumably offer better products at lower prices. But a decline in market share doesn’t necessarily mean you should avoid investing in a particular company. You can produce big returns if you identify companies that reposition and strengthen their product offerings to reverse a market share decrease.

6. P/E ratio

This section tells you that Starbucks sells at a P/E (price-to-earnings ratio) of NMF which means “not meaningful” because of its recent stock price and earnings which happened to be negative due to the COVID-19 pandemic. Based upon Value Line’s estimate of Starbucks earning $2.90 per share next year, the stock is selling at a P/E of 26.7.7. Capital structure

This section summarizes the amount of outstanding stocks and bonds that the company possesses. Remember that when a company issues these securities, it receives capital (money). The most useful number to examine in this section is the company’s debt. If a company accumulates a lot of debt, the burden of interest payments can create a real drag on profits. If profits stay down for too long, debt can even push some companies into bankruptcy.The figure shows you that Starbucks has an outstanding debt of $16.8 billion. But how do you know if this is a lot, a little, or just the right amount of debt?

Possessing a larger cushion to cover debt is more important when the company’s business is volatile. You can calculate total interest coverage, which compares a company’s annual profits to the yearly interest payments on its total debt. This number tells you the number of years that the company’s most recent annual profits can cover interest on all the company’s debt.

For example, if a company has a total interest coverage of 4.5x, the company’s most recent yearly profits can cover the interest payments on all debt for about 4-1/2 years. Starbucks’ most recent annual profits of $3,492 million exceed its interest payments of $700 million by a factor of nearly 5 to 1. Warning signs for total interest coverage numbers include a steep decline in this number over time and profits that cover less than one year’s worth of interest.

8. Current position

This section provides a quick look at how the company’s current assets (assets that the company can convert into cash within a year relatively easily) compare with its current liabilities (debts due within the year). Trouble may be brewing if a company’s current liabilities exceed or are approaching its current assets.Some financial analysts calculate the quick ratio. The quick ratio ignores inventory when comparing current assets to current liabilities. A company may have to dump inventory at a relatively low price if it needs to raise cash quickly. Thus, some analysts argue, you need to ignore inventory as a current asset.

9. Annual rates

This nifty section can save wear and tear on your calculator. The good folks at Value Line calculate rates of growth (or shrinkage) on important financial indicators, such as sales (revenues) and earnings (profits) over the past five and ten years. This section also lists Value Line’s projections for the next five years.Projections can prove highly unreliable, even from a research firm as good as Value Line. In most cases, the projections assume that the company will continue as it has in the most recent couple years.